Dreams of leaving the daily grind and living a life of wealth are widespread, but for many, they stay just that—dreams. Robert T. Kiyosaki, on the other hand, was determined to see his dreams come true. Inspired by his own father’s financial troubles, Kiyosaki began on a wealth-creation quest, learning the principles that govern financial success. In this post, you will learn about Kiyosaki’s basic ideals and the key ideas outlined in his book Rich Dad’s Cashflow Quadrant.

The various methods of generating income can be categorized into four distinct groups.

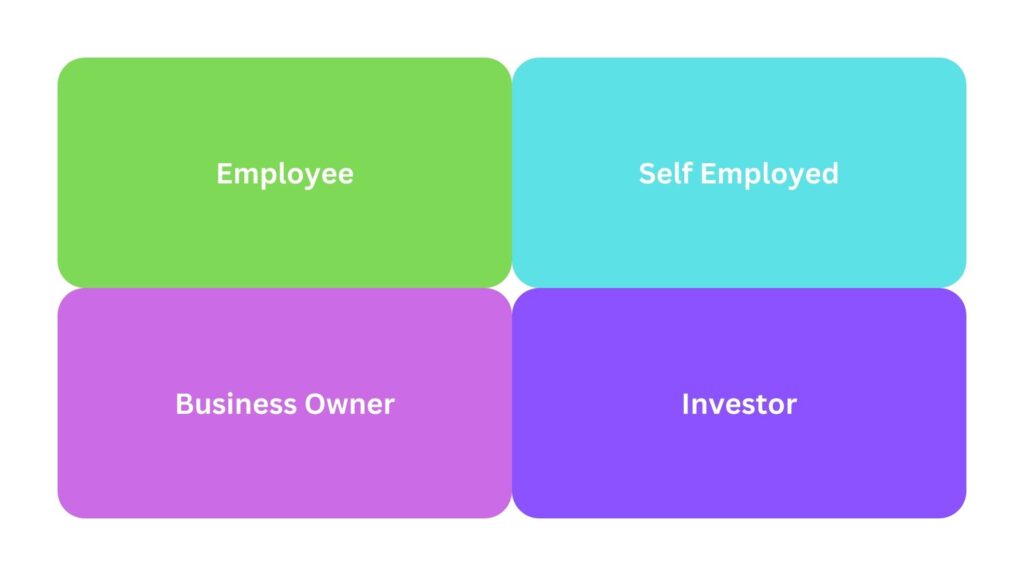

The various ways of producing money can be classified into four quadrants. Imagine sketching a ‘plus’ sign on a piece of paper. The two lines that partition the room create four distinct regions. These zones, known as quadrants, serve as the cornerstone for our society.

Each quadrant has a unique label: E, S, B, and I. The ‘E’ is for employee, the ‘S’ is for self-employed, the ‘B’ is for business owner, and the ‘I’ is for investment.

You are classified into one of these quadrants based on your source of income. Throughout your career, you may make money from one, two, or all of them.

For example, consider an American medical doctor. They may make a living as employees by working for a large hospital, an insurance firm, or the government in the public health sector. This can be accomplished by working a nine-to-five job.

On the other hand, the same doctor could choose to be self-employed and establish their own private practice. They would open an office, hire employees, and grow a private patient base. While this would still be difficult, they would have greater autonomy.

As a third alternative, they may become company owners by opening their own clinic and hiring other doctors. They would most likely pay someone else to run the business, allowing them to own the clinic without having to work there themselves. They could even continue working as a medical professional while owning a non-medical-related business.

As a highly paid doctor, they may have investable income. To accomplish this, they could invest in stocks or real estate while practicing medicine, running a clinic, or managing a business.

These quadrants mirror our society’s fundamental structure, and each requires unique abilities and personal attributes. While there is no right or wrong answer, some people are pleased with whatever quadrant they find themselves in.

If you want financial freedom, you must leave the E and S quadrants and move into the B and I quadrants, or from working to owning. This will be detailed more in the following section.

Rich Dad’s Cashflow Quadrant

Education and hard work alone are not sufficient to achieve financial independence.

Robert Kiyosaki grew up in Hawaii with two father figures who had quite different lifestyles and orientations to work and money. His biological father, who held a coveted government post while being well educated and respected, was often swamped with work, leaving little time for his family or personal hobbies. He trusted the common wisdom that hard effort alone would result in financial security, ignoring the importance of financial education and investment.

Mike’s father, a self-made entrepreneur and investor, had both time and money. He began investing in real estate at a young age and developed a profitable hotel business, producing passive income that enabled him to live a more balanced life. Despite not having a formal education, he had a thorough awareness of financial concepts and took deliberate decisions to leave the regular nine-to-five grind.

The main conclusion from Kiyosaki’s experiences is that financial freedom is reached not only via hard effort and education, but also by improving financial literacy and making sound investment selections. While education and working hard might lead to professional achievement, they are not the only paths to financial security. Investing in passive income-generating assets, such as real estate, can provide you the freedom to pursue your own interests and live a more satisfying life.

Rich Dad’s Cashflow Quadrant

Hard work is essential, but smart work is where true excellence emerges.

While visiting his friend Mike, the author’s “rich dad” told him a story that would shape his financial education and highlight the clear difference between people who operate in the E and S quadrants and those who thrive in the B and I quadrants.

The plot revolves around two village contractors, Ed and Bill, who are tasked with providing the hamlet with water. Ed, representing the conventional way, chose hard work, painstakingly bringing buckets of water from a nearby lake to replenish the village’s tank. Despite receiving a salary, his efforts were time-consuming and stressful.

In contrast, Bill, who embodies the ideals of financial intelligence, chose a strategic approach. Instead of using raw force, he formulated a strategy, formed a corporation, obtained investors, assembled a team, and built a stainless steel pipeline that connected the community to the lake.

Bill quickly expanded his network, bringing clean, economical, and easily accessible water to adjacent settlements. His approach, once in motion, provided passive income, allowing him to enjoy financial independence. Ed, bound to his physical labor, worked constantly, trying to make ends meet.

In the end, Bill sold his thriving pipeline business and retired in wealth and prosperity. Ed, on the other hand, watched his children depart the community, unconcerned about his antiquated water-bucket venture. This tragic story emphasizes the fundamental difference between working hard and working wisely. Those that embrace techniques and systems, such as Bill, can break free from the constraints of the traditional employment and attain financial independence, whereas Ed is locked in a cycle of manual labor and restricted options.

Rich Dad’s Cashflow Quadrant

In today’s uncertain economic climate, it is crucial for individuals to take responsibility for their own financial well-being.

In today’s Information Age, the concept of a secure career with a government pension is obsolete. The traditional adage of working hard and relying on the government for security no longer applies. Instead, we must take responsibility for our financial destiny, shifting into either the B or I quadrants: Large corporate ownership or investment.

Our grandparents had the luxury of anticipating government assistance, but the reality today is vastly different. With an estimated 100 million Americans reliant on government aid, the expense is simply unsustainable. Furthermore, boosting taxes to pay these responsibilities will just push the wealthy to countries with lower tax rates.

Robert Kiyosaki, the author of Rich Dad, Poor Dad, learnt this lesson directly from his two father figures. His biological father, a government official, was reliant on government security until he lost his job due to a political disagreement. Unable to navigate the B and I quadrants, he failed in his entrepreneurial pursuits and went bankrupt.

In contrast, Kiyosaki’s “rich dad” established a passive income scheme that provided a consistent supply of cash, protecting him from financial trouble throughout his life. The objective, Kiyosaki says, is to learn to own assets and generate income that is independent of your own labor.

In today’s volatile environment, relying on government assistance is a risky undertaking. We may take charge of our financial future and achieve long-term security by knowing the four quadrants’ ideas and implementing wealth creation tactics.

Rich Dad’s Cashflow Quadrant

People with different motivations and preferences tend to gravitate towards different quadrants.

The four quadrants attract people with diverse motivations and attitudes on work and money.

Employees (E quadrant) desire stability and security, valuing a consistent wage and benefits. They are motivated by a fear of financial insecurity and destitution. Their work ethic is frequently driven by a desire for a consistent paycheck rather than a passion for their profession.

Self-employed people (S quadrant) value independence and frequently believe they can do a better job than others. They are motivated by a desire to control their own money and avoid being governed by their bosses. Their work ethic is frequently motivated by a love for their art and a desire to be their own master.

Business owners (B quadrant) are expert delegators who surround themselves with competent people from many professions. Their key ability is to build and manage revenue-generating processes, while they monitor the whole operation. They are motivated by the desire to produce long-term wealth and worth.

Investors (I quadrant) take calculated risks, similar to gamblers, but with a more informed perspective. They aim to understand the risks associated with their ventures before investing funds. Great investors, such as Warren Buffett, excel at balancing risk taking with extensive research and analysis. They are motivated by the ambition to build riches and achieve financial freedom.

Understanding each quadrant’s unique personalities and motives can help people identify their own tendencies and potential paths to financial success.

Rich Dad’s Cashflow Quadrant

Entrepreneurship and investment are the most reliable paths to financial independence.

If you’re reading this, you probably want financial freedom – the ability to pursue your interests, whether it’s traveling the world, collecting art, or diving with manta rays. But how can one acquire this level of financial independence? By taking the same path as many of the world’s wealthiest individuals: shifting from business ownership to investment.

Bill Gates, Rupert Murdoch, and Warren Buffett, all well-known billionaires, began their careers as successful businessmen. They then used their business knowledge and cash to become savvy investors, accumulating large fortunes.

The rationale for this transition is straightforward: to accumulate wealth, one must accumulate money. The most effective way to do so is to invest, whether in stocks, funds, or real estate. However, successful investing necessitates a consistent flow of funds and time. The easiest method to accomplish this is to create a business that will generate revenue even when you are not actively involved.

Just as Kiyosaki’s “rich dad” built his hotel empire, you may create an autonomous business system that allows you to invest higher sums of money without sacrificing your time and energy. This, in turn, can catapult you from the financial stability of business ownership to actual financial freedom through large-scale investing.

There is another strong incentive to take this path: your company expertise will prepare you to be an extraordinary investor. Through your business efforts, you’ll obtain a thorough grasp of effective business concepts, allowing you to make smart investment decisions with long-term rewards.

In contrast, attempting to go immediately from the E and S quadrants (employee and self-employed) to the I quadrant (investor) without a solid foundation of business experience sets you up for investment failure. Your investments are more likely to fail if you don’t comprehend what makes up a successful business system. Furthermore, without the financial backing of a huge corporation, your investment options will be limited, raising risk.

If you aren’t interested in starting your own business but want to invest, get to know the many types of investors. This will provide you the knowledge you need to make sound judgments and decrease the possibility of costly mistakes. In the following section, we will look at the various investor personalities and the techniques they deploy.

Rich Dad’s Cashflow Quadrant

Investors can be categorized into five distinct groups.

Investing can be a difficult task, but with the proper education and strategy, anyone can become a successful investor. Here are the five main types of investors, ranging from beginners to the likes of Warren Buffett:

Zero-Financial-Intelligence Level

This category includes the bulk of the people, who may be financially illiterate or have a high level of debt. To become investors, they must first address their financial basics and gain control over their spending and saving habits.

Savers-Are-Losers Level

These people assume that just saving money is sufficient for financial security. However, in today’s low-interest economy, simply storing money in a bank account does not provide significant returns. As the 2008 financial crisis illustrated, even bonds, which are frequently thought to be secure investments, can lose money.

I’m-Too-Busy-Investor

These individuals entrust their investment decisions to financial consultants, expecting for expert advice. While this strategy may appear to be convenient, it contains considerable hazards. Many investors lost money during the 2008 meltdown as a result of poor advise from their “experts.” It is critical to select a financial advisor with a solid track record and a thorough understanding of your financial objectives.

I’m-A-Professional Level

This group represents the first true investors. They take the initiative to educate themselves on investments, perform extensive research, and make sound decisions. This method results in more concentrated investments and a solid financial base.

Capitalist Level

This is the Warren Buffett level, in which people not only invest their money but also start profitable businesses. They then utilize their funds to make riskier but perhaps more profitable bets. While this road can lead to significant wealth, it is also the most difficult, requiring strong business knowledge and risk tolerance.

If creating a corporate empire isn’t your goal, the “I’m-A-Professional” investor level is a more realistic goal. By educating yourself and taking control of your finances, you can improve your chances of financial success.

Rich Dad’s Cashflow Quadrant

Money can evoke intense emotions that we should seek to understand and control.

The author delves into the irrational behaviors that money often provokes in people. Drawing from personal experience, he illustrates how a snake phobia can prevent someone from acting rationally, even in life-threatening situations. This analogy is used to highlight the impact of investment anxiety, which can lead even well-educated individuals to make poor financial decisions.

To succeed financially, the author argues, it is essential to confront these fears and adopt a logical mindset toward money. Comparing it to the game of Monopoly, he explains that the goal is to accumulate as many profitable “houses” as possible, whether in the form of rental properties or stocks. Overcoming financial fears, he asserts, is key to achieving success.

Sharing his own journey, the author recounts how he and his wife faced homelessness in their pursuit of financial independence. Despite the challenges, their perseverance paid off, enabling them to build a thriving business and attain millionaire status within just four years.

Rich Dad’s Cashflow Quadrant

Achieve financial success by embracing the power of small, consistent actions and maintaining a long-term perspective.

Financial freedom is a long-term goal, and chasing immediate wealth is a bad strategy. Successful people amassed their riches over time, not suddenly. Instead of falling victim to get-rich-quick scams, concentrate on making little, consistent progress and planning for the future.

Short-term thinking frequently results in financial overextension. Remember, Rome was not built in a day; successful investors began small and grew progressively. Warren Buffett, for example, started selling chewing gum door to door.

In today’s turbulent Information Age, job security is unsure. Even if you now have a well-paying job, you should not rely completely on it for money. Diversify your portfolio with long-term compound investments. This entails starting small and reinvesting your income or profits. Albert Einstein famously described compound interest as the eighth wonder of the world.

Investing in your education will help you gain more financial literacy. Understanding the stock market or the real estate industry can provide useful insights and protection against market swings. With a solid financial foundation, you’ll be better prepared to face the challenges of the future and attain financial independence.

Source

This book summary of Rich Dad’s Cashflow Quadrant was inspired by Blinkist.

In today’s fast-paced world, it can be challenging to find the time to read all the books you want to learn from. But thanks to Blinkist, you can now devour the key ideas from thousands of nonfiction bestsellers in just 15 minutes per title.

Whether you’re a lifelong learner, a busy professional, or simply curious about the world around you, Blinkist is the perfect tool for expanding your horizons and becoming a more informed and well-rounded individual.

Start your Blinkist journey today and discover the transformative power of knowledge. Or read more book summary’s from me here.